The latest data from Knight Frank shows that investor appetite for purpose-built student accommodation (PBSA) was strong in H1, despite the sector being adversely impacted by the pandemic, with restrictions limiting international travel and disrupting study for a large proportion of students. The sector is in a strong position to bounce back as face-to-face teaching resumes and a pursuit for the ‘university experience’ incites students.

Total investor spending for the first half of the year reached almost £2bn, as deal volumes rose, and investors looked beyond short-term disruption. Cumulative deal volumes to the end of June were 47% higher than the same period last year and 4% higher than in 2019. Recent UCAS data shows increased optimism for the scale of demand this autumn, with year-on-year rises evident from both UK and overseas applications.

Summarising the uptick in investment transactions, Knight Frank believe it shows that investors, ‘have confidence in the sector’s ability to deliver long-term, stable income streams. It also reflects a wider pivot which has taken place over the last 18 months, from institutional investors towards residential assets across all age groups. Rising student numbers and ongoing low supply ratios in many university cities are also driving investor demand for PBSA.’

The newly compiled Commercial Property Survey from the Royal Institution of Chartered Surveyors, for Q2 2021, clearly highlights an improvement in overall market sentiment, with 56% of respondents currently feeling that market conditions are consistent with an upturn, this is an increase from 38% in Q1 this year.

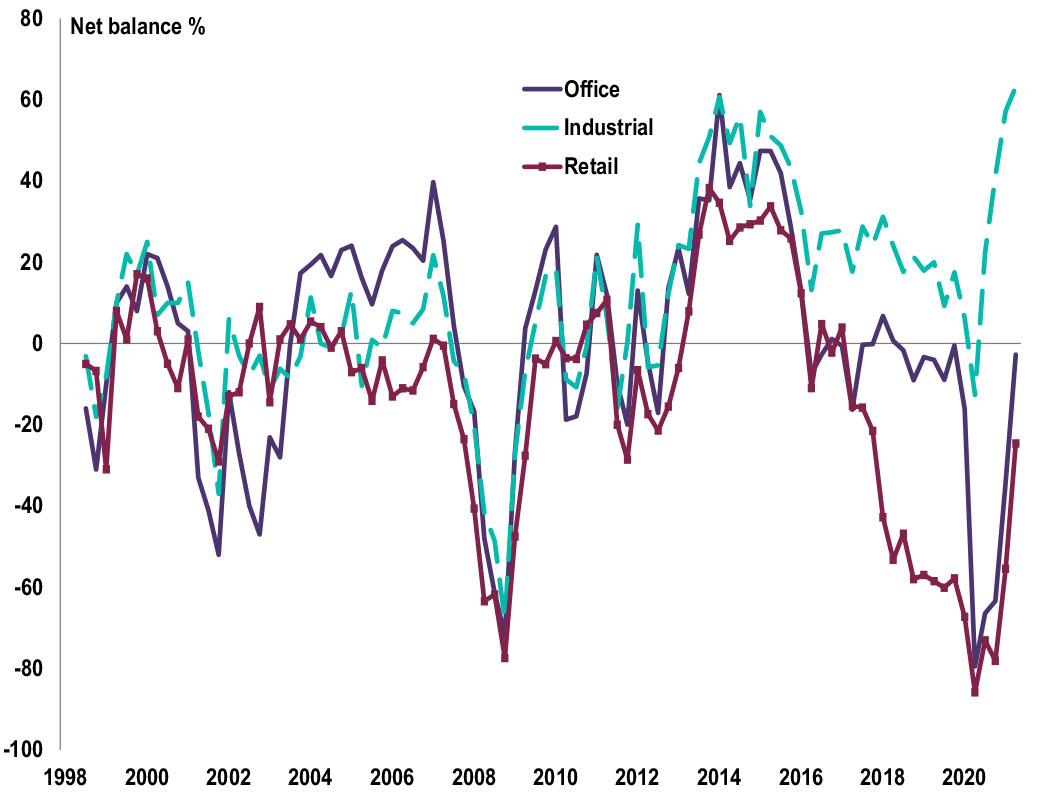

The industrial sector continues to experience sharp growth in interest from both investors and occupiers. Respondents to the quarterly survey refer to a continuation in the sharp contraction in availability of leasable industrial space, with the net balance falling deeper into negative territory at -48%, compared with -39% in Q1. Over the next year, respondents expect strong industrial capital value growth across all UK regions.

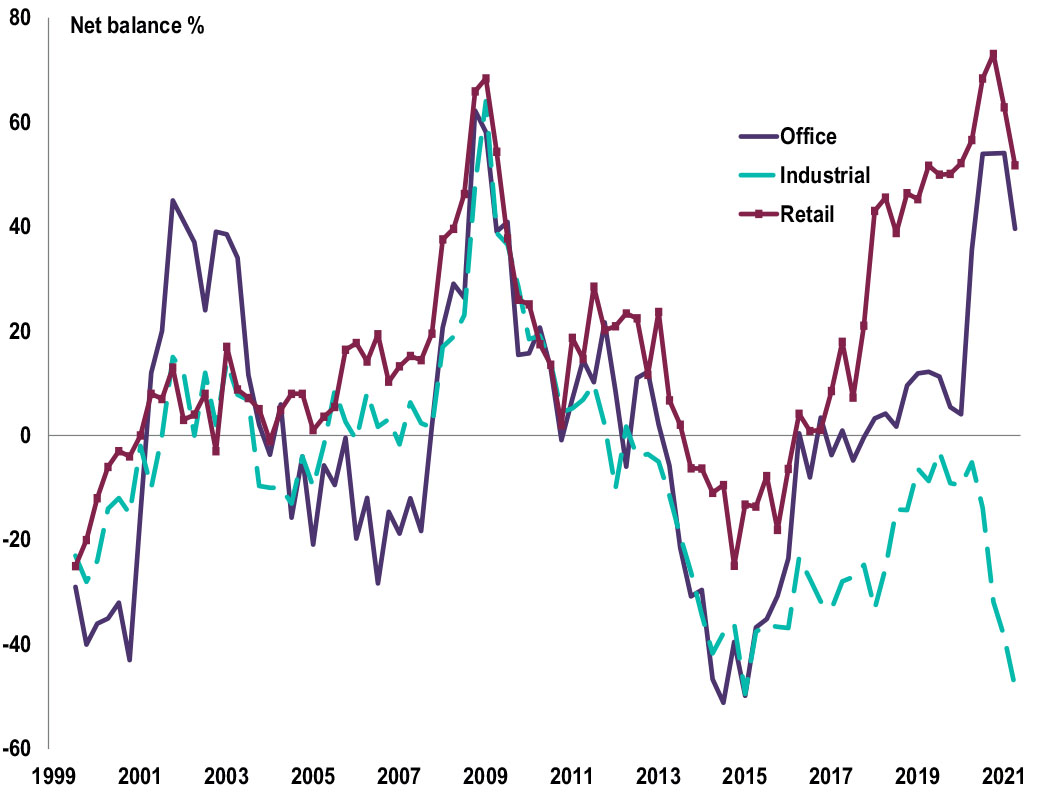

Encouragingly, trends in demand in the office sector seem more stable than the previous quarter. Although both secondary and prime retail values are predicted to decline, projections are less negative than in previous surveys. Retail availability continues its upward trajectory. Across the retail and office sectors, returning net balances of +52% and +40% respectively in Q2, were recorded.

Demand varies widely at a sector level, with current sector net balances measuring +63% for industrials (versus +57% in Q1), -3% for offices (versus -34% in Q1) and -25% for retail (versus -55% in Q1).

In what the report declared a ‘noteworthy development‘, capital value projections are now only ‘marginally negative for hotels‘, with the latest net balance shifting significantly from -47% in Q1 to -4% in Q2.

| Rising student numbers and ongoing low supply ratios in many university cities are also driving investor demand for PBSA |

| Region | No. properties | AVG. asking price |

|---|---|---|

| London | 1,324 | £1,550,639 |

| South East England | 1,143 | £2,074,320 |

| East Midlands | 745 | £1,007,808 |

| East of England | 733 | £633,795 |

| North East England | 777 | £349,285 |

| North West England | 1,270 | £446,614 |

| South West England | 1,516 | £536,991 |

| West Midlands | 1,137 | £488,318 |

| Yorkshire and The Humber | 1,117 | £316,941 |

| Isle of Man | 51 | £486,457 |

| Scotland | 1,102 | £304,831 |

| Wales | 755 | £422,476 |

| Northern Ireland | 26 | £412,121 |

Source: Zoopla, data extracted 19 August 2021

Source: RICS, UK Commercial Property Market Survey, Q2 2021

Source: RICS, UK Commercial Property Market Survey, Q2 2021

All details are correct at the time of writing (19 August 2021)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.